The Low Cost of Inaction: Don’t Just Do Something, Stand There!

/

“We already see resurgent the age-old frailty of the investor – that his money burns a hole in his pocket.” Thus wrote Benjamin Graham in his seminal work on value investing, Security Analysis, written in 1934. Yet those words are just as relevant in today’s investment climate where many once again think that all they need to do to succeed in investing is to buy stocks of glamorous, high-growth companies. Valuation is once again perceived to be only of passing interest, a topic focused on by those unsophisticates that have not evolved to a higher level of understanding, one that allows the true investing gurus to pinpoint the future of rapidly growing companies 15+ years out.

If you have been paying any attention to the rising stock market in the last couple of years, you might be tempted to succumb to this siren-song and relax your investment criteria in order to join those appearing to make money quarter after quarter in high-expectation growth stocks. Don’t… at least not until you read this article.

Value Investing Works…

Statistically inexpensive “value” stocks have on average outperformed statistically expensive “glamour” stocks across the board over the long-term

The cheapest decile of stocks has outperformed the median stock by ~ 2% per year

… But Value Investing Does Not Work All the Time

Fifteen years ago, as a young analyst, I attended a conference at Harvard on Behavioral Finance. During one of the sessions, a well-known value investor presented evidence that value investing has produced superior returns over all rolling 10-year periods during the timeframe that he studied. I came up to him after his talk, and asked – if value investing works so well, why doesn’t everyone do it? He smiled at me knowingly and explained that while value investing works over most long-term periods, it frequently doesn’t always work in the short-term. There are plenty of 3-year periods when value investing produces inferior returns, and most market participants don’t or can’t have the time horizon that is sufficiently long to be able to look through that. They will either get fired, lose their clients, or if they are investing their own capital, lose the confidence in their process while they wait for the period of underperformance to end.

In other words: Value investing works over the long-term exactly because it doesn’t work all the time. If it worked all the time, it would have been arbitraged away long ago by people programming computers to invest large amounts of money based on its principles. However, because of intermediate-length periods when value investing doesn’t work, and most investors’ lack of a long-term time horizon, this hasn’t happened and value investing remains one of the few constants in a changing investment landscape. Most people just can’t stomach periods of underperformance. (For more on this topic, see How and Why to Be a Long-Term Investor).

The Math of Waiting for Attractive Opportunities is Very Forgiving

We are frequently told not to time the market. I believe that is right for those whose only equity investing option is the market. So if you are pursuing a dollar-cost-averaging approach using low-cost index funds (something I think many would benefit from as I wrote in Why Passive Investing Is an Excellent Default Choice – an Active Investor’s View), by all means continue with that approach. However, if, like me, your goal is to find individual under-valued securities in which you invest only when they offer a large margin of safety, then the following analysis is highly relevant.

Hypothetical Scenario #1

Option A: Invest in the market immediately. Assume 8% long-term (70-year) nominal annual returns (might be generous from the current starting point)

Option B: Hold cash for 3 years, then invest in an attractive investment with an IRR typical of ones that I seek (13%)

Internal Rates of Return (IRRs): Option A: 8%; Option B: ~ 10%

Hypothetical Scenario #2

Option A: Invest in the market immediately. Assume 7% nominal annual returns for 8 years (a generous estimate from the current starting point)

Option B: Hold cash for 3 years, then invest in a security with a Price/Value ratio of 65%. Assume that it takes 5 years for the Price/Value gap to close, with value growing at the discount rate I use to estimate value (10%)

Internal Rates of Return (IRRs): Option A: 7%; Option B: ~ 12%

The Current Opportunity Set Is Not Attractive

There are two ways to look at the attractiveness of the market: bottom-up and top-down. To a concentrated value investor such as me, the former approach is much more relevant because even if the whole market were grossly overvalued, it could be quite possible that enough attractive opportunities exist to put together a portfolio offering excellent potential returns with a large margin of safety. An example is the Tech bubble of 1999-2000, when overall valuations were very high, but there existed many opportunities in “old-world” industries that didn’t get caught up in the speculative craze that affected technology, telecommunications and media stocks.

The most relevant measure of bottom-up investment opportunities is what each investor can find that fits their process. However, I thought as a broader measure I would present recent data from Morningstar, which:

1. Takes an intrinsic value approach to valuing stocks, just as we do

2. Is focused on analyzing business quality and each company’s competitive advantage

3. Has done this for a large, 1,800+ universe of companies which should be reasonably representative of the broad opportunity set

Source: Morningstar Premium Stock Screener (http://www.morningstar.com)

Out of 1,807 stocks that Morningstar has analyzed, 1,177 get either its ‘Narrow Moat’ or ‘Wide Moat’ rating. This means these are companies that Morningstar believes possess some degree of sustainable competitive advantage

Of that universe, only 17 companies are currently priced at 70% or less of Morningstar’s estimate of intrinsic value

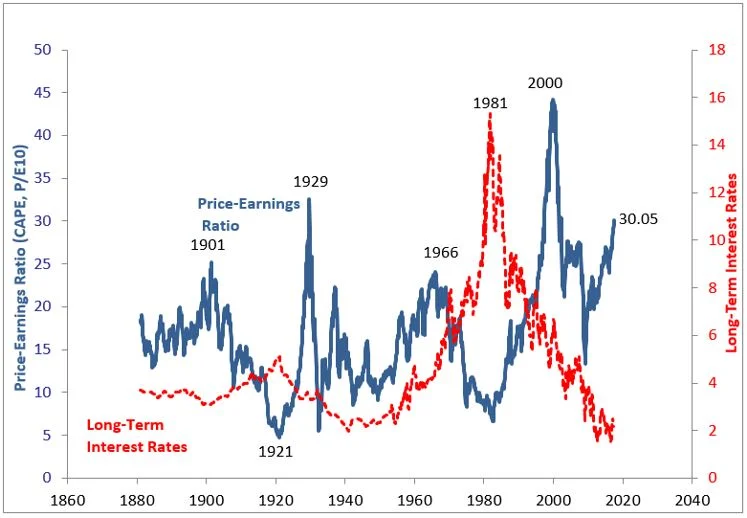

Even though I find the bottom-up approach to assessing investment opportunity to be much more useful than the top-down approach, let’s take a look at one of the best top-down indicators, Robert Shiller’s Cyclically Adjusted P/E (CAPE) ratio:

Based on this perspective, the only way the market is not substantially above sustainable valuation levels is if current long-term interest rates permanently remain at these levels. Even then, the current valuation levels are higher than some other time periods with similarly low interest rates.

Nobody knows what the right valuation is for the market, and I spend no time trying to answer questions such as that. However, we do know that over the long-term, valuation levels and interest rates have tended to revert to the mean and that we are far above that mean with respect to market valuations. From these levels, it is very hard to conclude that the annualized US market returns over the next decade are likely to be anything better than single-digits, with a substantial possibility of mid-single digit or worse annualized rate of return over that period.

Why Aren’t There More Investment Managers Willing to Wait for the Right Investment Opportunities?

The standard refrain from mutual fund managers and institutional investors goes something like this: our clients already made the asset allocation decision to invest in equities, so now it is our job to be fully invested and find the best of what is currently available, regardless of absolute valuation levels. They then typically add that missing out on even a few of the stock market’s best days each year has been shown to have a large negative impact on annual performance. I believe this is flawed logic:

I do not think that most clients would want their managers investing in equities irrespective of the possibility for permanent capital loss or potential long-term returns

Clients should give money to equity managers so that those managers can achieve attractive long-term returns while guarding against the risk of permanent capital loss over the long-term

This does not necessarily imply that a manager needs to be fully invested all of the time, particularly if doing so could mean endangering clients’ capital or locking it in at sub-par rates of return

Managers do need to achieve both an attractive absolute rate of return above inflation as well as comfortably exceed a low-cost passive index alternative over a full market cycle

Clients entrust us with their capital in part because they believe that we have expertise that they do not. Therefore, as investment managers, we shouldn’t argue that ‘the clients made us do it’ as justification for committing their capital on terms that we normally would not find attractive. Sitting on the sidelines waiting for opportunities that meet our quality and valuation criteria involves the risk of appearing out of step with a rising market, which in turn puts investment managers at risk of losing clients, bonuses or jobs. However, as fiduciaries it is our job to reject the old cliché that it’s far better to fail conventionally than succeed unconventionally and do what we believe to be in the best long-term interest of our clients. It’s important that when there are not enough attractive investments that combine sufficient quality with a large discount to intrinsic value that we follow the admonition: don’t just do something, stand there!

If you are interested in learning more about the investment process at Silver Ring Value Partners, you can request an Owner’s Manual here.